Ontario new-build cash to close: why the rebate is not the wire amount

Ontario's proposed new-build HST rebate has a simple headline: eligible homes could see relief up to $130,000. That headline is useful. It is not the same thing as the amount you may need to wire before closing.

If you are buying a new build, the number that matters on closing day is usually a ledger. The rebate is one line. The rest of the ledger can include deposits still owed, land transfer tax, Toronto municipal land transfer tax, Ontario PST on CMHC insurance, legal and title costs, Tarion or warranty amounts, development charges, utility charges, reserve-fund contributions, builder adjustments, and credits.

The practical question is not only "what is my rebate?" It is "how much cash might I need available when the lawyer asks for funds?"

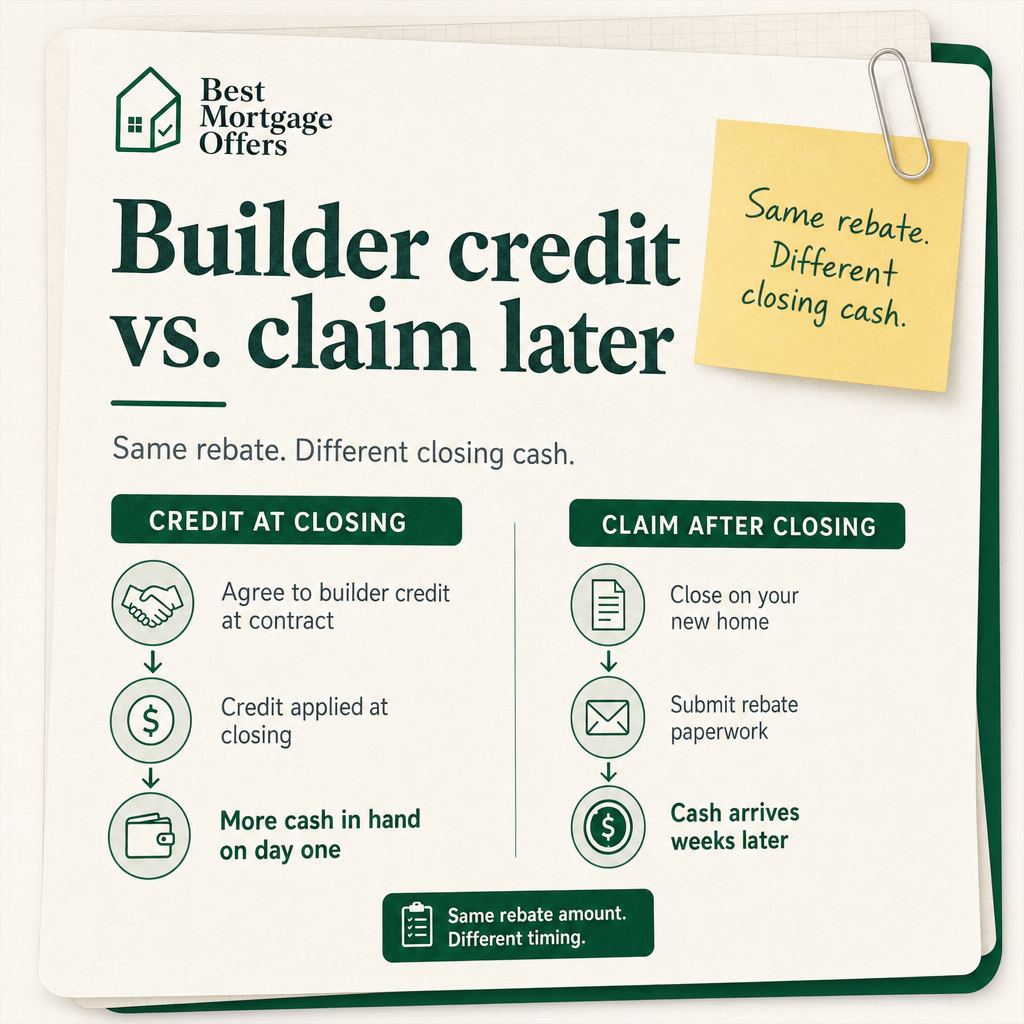

Start with the wire amount

A rebate can help only if it lowers the amount due at the right time. If the builder credits the rebate on the statement of adjustments, your closing cash may fall. If you claim the rebate later, the rebate may still be valuable, but it may not help before the lawyer asks you to send funds.

| Scenario | What to look for | Cash effect |

|---|---|---|

| Builder credits the rebate | The closing worksheet shows a rebate credit or assigned rebate. | Your wire may be lower. |

| You claim later | You close first and apply after closing, where eligible. | You may need more cash up front. |

| Treatment is unclear | The agreement or worksheet does not say how the rebate is handled. | Run both cases until the builder or lawyer confirms it. |

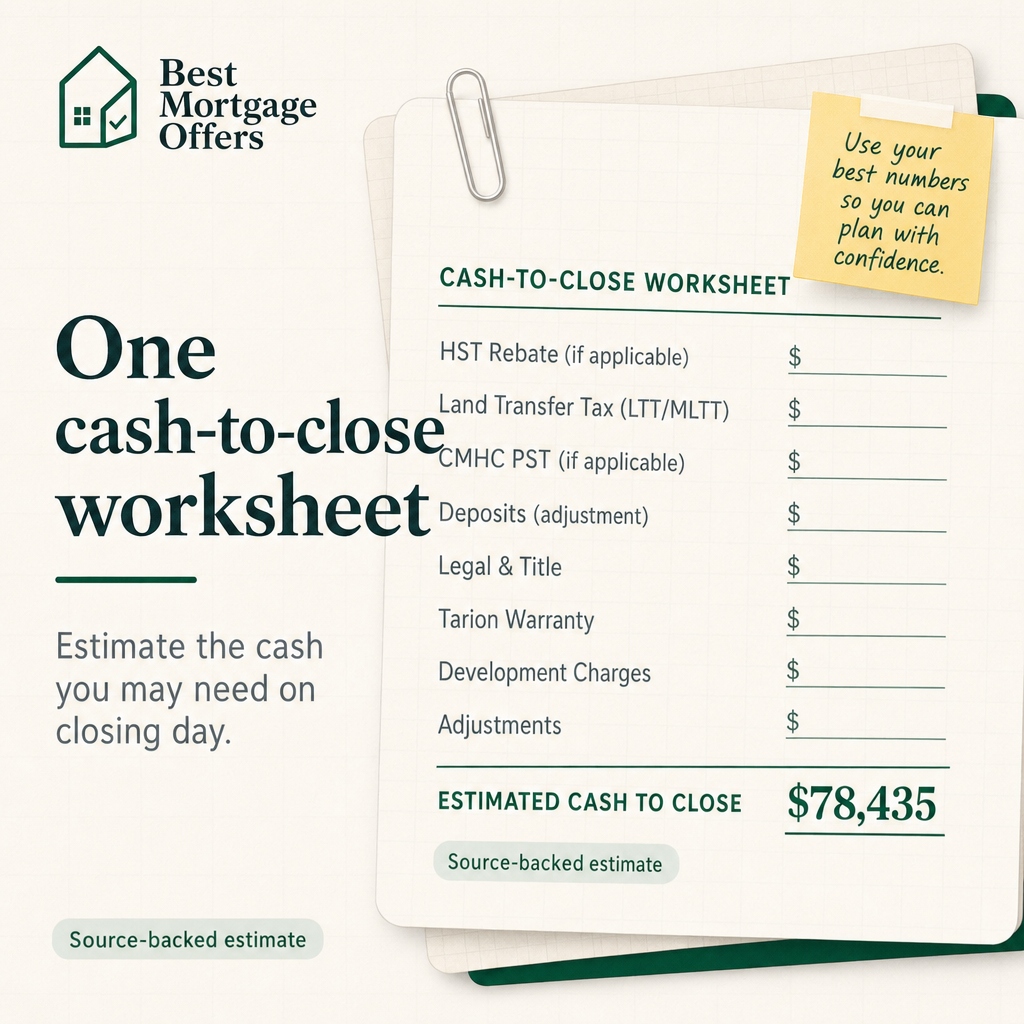

Example: one rebate, more than one closing ledger

If you are buying a $950,000 Toronto new build with 10% down and $50,000 already paid as a deposit, the rebate is not the only planning number. The ledger may look more like this before final builder paperwork arrives:

| Cash-to-close line | Example amount | Why it matters |

|---|---|---|

| Down payment still needed | $45,000 | A deposit reduces what you still owe, but it does not erase the rest of the down payment. |

| Ontario and Toronto land transfer tax | $22,475 | Toronto purchases can face both Ontario LTT and Toronto MLTT, less any eligible first-time buyer rebates. |

| Ontario PST on CMHC insurance | $2,120 | The CMHC premium can usually be added to the mortgage, but Ontario PST on that premium is normally paid in cash. |

| Legal, title, Tarion, builder extras, and adjustments | $8,840 | These are planning allowances until the lawyer and builder provide the final documents. |

Where to find the numbers

You do not need every final document to start. You do need to know where each number will eventually come from.

- Agreement of purchase and sale: price, agreement date, purchaser names, deposit schedule, GST/HST wording, and rebate assignment wording.

- Deposit receipts: cash already paid, separate from the total down payment you plan to make.

- Mortgage commitment: down payment, insured-mortgage status, and mortgage insurance assumptions.

- Tarion, HCRA, or builder documents: warranty context, development charges, utility charges, and important dates.

- Statement of adjustments: final credits, charges, builder adjustments, and whether a rebate appears at closing.

- Lawyer's funds request: the final wire amount.

Rules to verify before relying on the estimate

The CRA first-time home buyers' GST/HST rebate is a federal path. CRA says full federal relief can apply up to $1 million for qualifying first-time buyers, with reduced relief before $1.5 million.

The existing GST/HST new housing rebate is separate. It can still matter for existing federal and Ontario rebate paths.

Ontario's 2026 HST relief should be treated as proposal-sensitive until final implementation details are confirmed. The Ontario backgrounder describes proposed temporary relief and timing tests, including agreement timing, construction-start timing, and substantial-completion timing.

Other cash lines have their own sources too: Ontario land transfer tax rates, Toronto MLTT rates and rebates, CMHC mortgage loan insurance costs, and Tarion enrolment fee information.

A better closing-cash workflow

Use the rebate estimate as one input, then keep moving toward the closing-cash number:

- Run a first estimate with price, location, dates, down payment, and deposits.

- Add first-time buyer details and primary-residence assumptions.

- Show both builder-credit and claim-later rebate cases if the treatment is unclear.

- Add legal/title costs, Tarion, development charges, utility charges, reserve-fund contributions, and occupancy fees as paperwork arrives.

- Ask your lawyer to confirm the final statement of adjustments and funds request.

The goal is not to replace professional advice. The goal is to make the lawyer's wire request less of a surprise.

Use the source-backed calculator: https://bestmortgageoffers.ca/#calculator

Read the full canonical guide: Ontario new-build cash-to-close HST rebate guide

Comments

Post a Comment